3 Contrarian Investment Strategies Worth Considering Today

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/T2LGZCEHBZBJJPPKHO7Y4EEKSM.png "3 Contrarian Investment Strategies Worth Considering Today")

Investors don’t need to look too hard to figure out what’s worked recently. The so-called Magnificent Seven stocks—Apple AAPL, Microsoft MSFT, Nvidia NVDA, Alphabet GOOGL, Amazon.com AMZN, Meta Platforms META, and Tesla TSLA—have been the poster children of US large-cap stocks’ success in recent years. Most everything else has fallen behind. The Magnificent Seven contributed to more than half the Russell 1000 Index’s returns over the past three years.

This is not normal. Global market allocations have shifted heavily to the US, especially its largest companies. While we know it’s not normal, it could be valid. But the world’s biggest companies tend to fall or fade away over time. The reasons are often unknowable ahead of time: We can’t write the obituary for another top company until after we see it happen.

Look at Cisco CSCO—the world’s most valuable company in the early 2000s. Its quick ascension in the decade leading up to the dot-com crash had Fortune magazine conclude, “No matter how you cut it, you’ve got to own Cisco.” A year later, Cisco had dropped 85%. It just recently worked its way out of this drawdown, so investors that bought Cisco stock in May 2000 would have barely broken even after 24 years.

This is the risk of buying a stock at extreme prices. It’s why many investors have remained wary of our current technology rally and the stretched valuations that came with it. But others are doomed to repeat their mistakes. Investors are compelled to participate in what’s winning. The future is cloudy, so recent past performance looks like a clear avenue to success.

Be it herding bias or fear of missing out, investors chase performance. Performance-chasing works in the short term like a self-fulfilling prophecy until most everyone considering buying a stock (or group of stocks) has already bought in. The roller coaster ratcheted its way up the hill but suddenly found itself with no new investors to climb up on. Then comes the drop.

Are we in a bubble that’s ready to pop? I don’t know. Often the factors that take down a company or an entire market are nearly impossible to conceive of beforehand. That’s why diversification matters.

Contrarian investors may be comfortable buying strategies that haven’t performed well in years. But others may be reticent to leave the safety of the herd, choosing to keep a close watch on the canary in the coal mine as their market-cap-weighted index fund becomes increasingly concentrated in a select few companies.

In this article, I’ll explain why alarm bells are ringing for me and how investors can adjust to current market conditions by enhancing their diversification, cashing out of what’s worked, and adding some strategies that are due for a rebound.

Canaries in the Coal Mine

Global stock performance has concentrated significantly in a handful of US stocks. Warnings about this phenomenon have come for years, but it has persisted and may continue for years to come. However, it has reached a point where I’m uneasy about the huge market share occupied by a select few. Here’s why (figures as of Aug. 22, 2024):

1) The market caps of Microsoft, Apple, and Nvidia make up more than 12% of the MSCI All Country World Index, an index that captures 85% of global investable stocks by market cap across 23 developed markets and 24 emerging markets (2,760 stocks in total).

2) A single product line is responsible for over half the revenues of two of those companies: Apple’s iPhone sales are about 50% of its revenue, and data center products make up 78% of Nvidia’s revenue. These products have an economic moat around them, but there’s a lot of money hanging on their success.

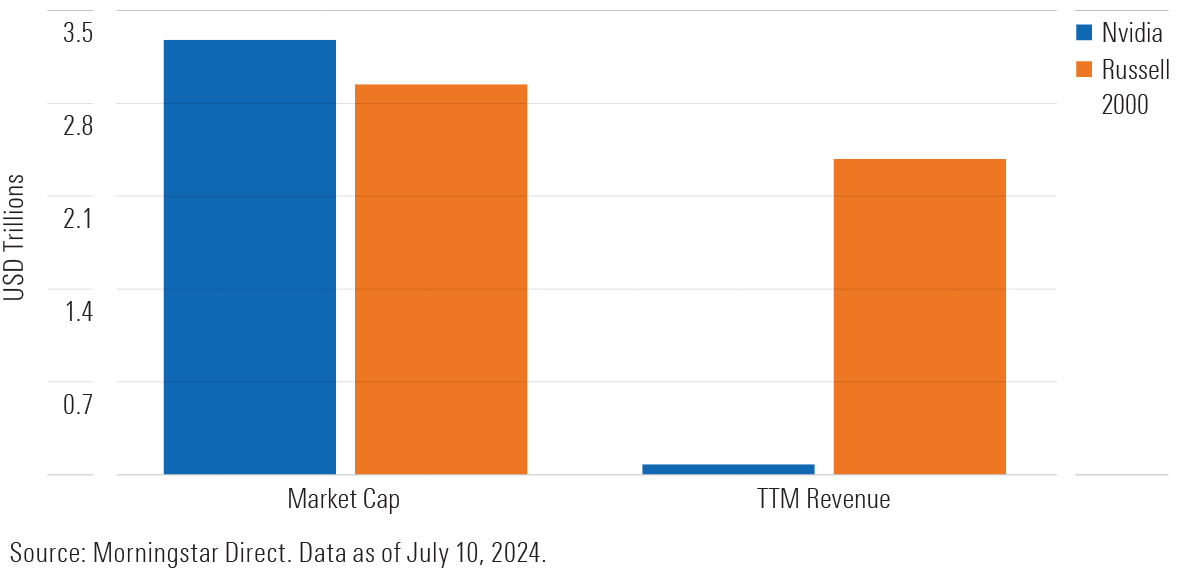

3) By market cap, investors near-equally value Nvidia and all 2000 stocks combined in the Russell 2000 Index. Nvidia’s market cap also exceeds the entire stock markets of the UK, Germany, and Canada.

4) NYU professor Aswath Damodaran reverse-engineered how big the artificial intelligence market and Nvidia’s share of it would have to be to justify the price. He found that the AI chip market would have to reach $500 billion—and Nvidia would have to have 80% of that market—to break even at Nvidia’s stock price of $45. As of Aug. 23, the stock price is now nearly 3 times higher at $129, meaning these calculations vastly understate the assumptions required for Nvidia to reach its current valuation.

Out-of-Favor Strategies May Flip the Narrative

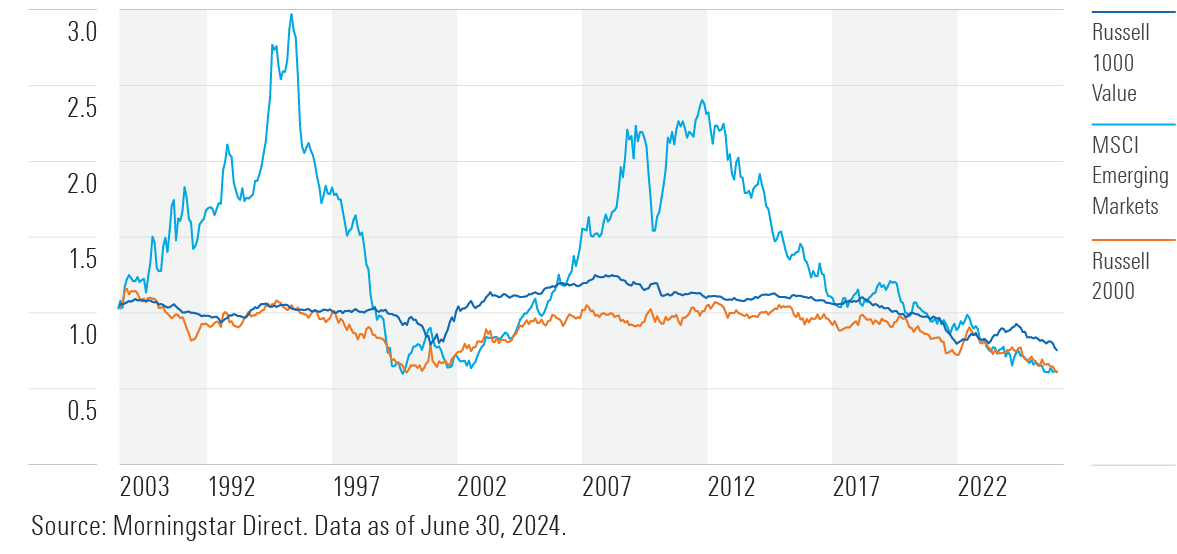

The successful run by US large caps leaves plenty of out-of-favor strategies for investors to tap into. Historical risk premiums like value and small size have not compensated investors lately. US large caps haven’t been this dominant relative to US large value, US small caps, and emerging markets since 2000. Now appears a good time to rotate into some of those out-of-favor strategies that stand to benefit should markets revert to their mean.

Why would value and small-cap companies make a comeback? Because investors have given up hope through a decade of underperformance. They no longer line portfolios in the way they did coming out of the global financial crisis. Because of the lack of demand, they are undervalued. As Corey Hoffstein of Newfound Research puts it, “No pain, no premium.” Patient value, small-cap, and emerging-markets investors have endured enough of the former to earn the latter.

My colleague David Sekera succinctly illustrates the opportunity for companies that characterize these risk factors in his third quarter stock market outlook. Holistically, value stocks are trading at a 15% discount to core stocks. Small caps are trading at a 25% discount to large caps. Perhaps most demonstrative, small-value stocks are trading at a 35% discount to large-core stocks.

Opportunities exist for investors to cash in on what’s worked and take some risk off by buying stocks with a greater margin of safety. Small-value stocks aren’t dependent on lofty expectations like Nvidia’s, giving them a lower bar for success and a shorter fall if things go awry.

Likewise, global portfolios’ allocation to international stocks has shrunk to make room for high-flying US stocks. The US’ share in the MSCI ACWI has grown to 64% as of Aug. 22. Like small-value stocks, there’s an opportunity to benefit from international stocks’ lack of popularity.

How to Add Out-of-Favor Strategies

Adjusting a portfolio to incorporate what’s out of favor doesn’t mean investors have to become small-value hermits. Switching from an S&P 500 exchange-traded fund to a total market ETF adds small-cap exposure, drops the average market-cap weight, and cuts the price/fair value of the holding by a small amount. It also reduces the S&P 500′s 33% stake in Magnificent Seven stocks by 4 percentage points. This small change can add diversification but won’t miss out much if current trends continue.

Below are ETF ideas with Morningstar Medalist Ratings of Gold and Silver for harnessing out-of-favor strategies:

All-In on Small Value

- Vanguard Small-Cap Value ETF VBR—Gold

- Dimensional US Targeted Value ETF DFAT—Silver

Large Core Tweaks

- Vanguard Total Stock Market ETF VTI—Gold

- Dimensional US Core Equity 2 ETF DFAC—Gold

Go International

- Avantis International Equity ETF AVDE—Silver

- Schwab Fundamental International Equity ETF FNDF—Silver

link