Overvalued, but Growth Intact Amid Strategic Investments

I have covered Meta Platforms Inc. (NASDAQ:META) many times before, and I’ve usually been bullish about the company. However, in this analysis, I think a neutral rating is more warranted because the valuation has become slightly overextended. The company’s year of efficiency gains have certainly culminated by now and moving forward, growth is likely to moderate toward more traditional levels and then slow further.

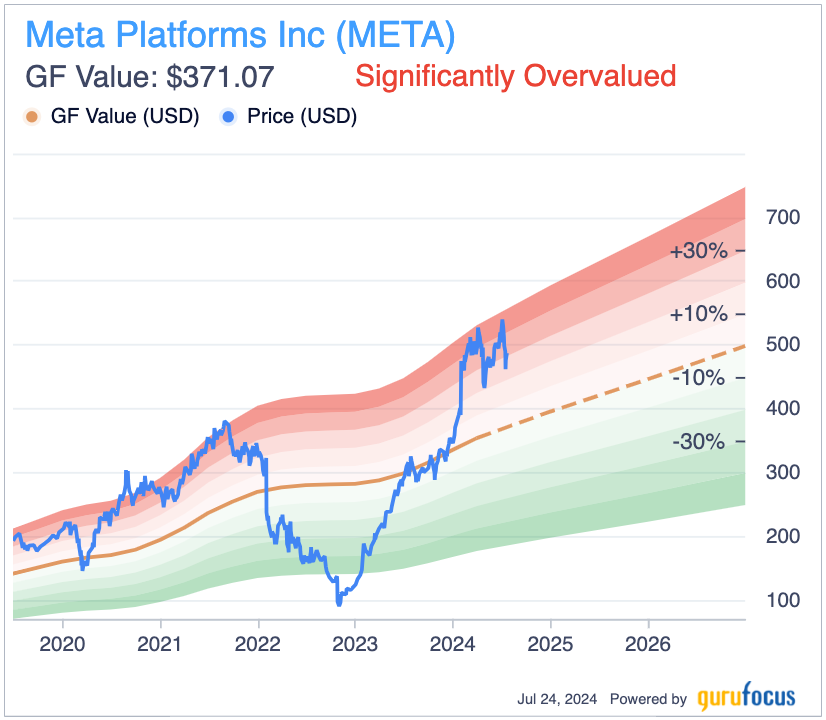

That being said, much of the near-term growth is already priced into the stock, which is made evident by the GF Value chart. However, I think long-term investors would be wise to continue holding Meta because it has recently issued a dividend, which I think is going to grow substantially over the next 10 years.

Meta is making heavy investments in artificial intelligence and the Metaverse, and management has noted these two technologies are vital to the company’s future growth. For instance, AI-driven content recommendations are boosting user interaction. Further, Meta has developed its own set of large language models. Based on this, I think it will become one of the leaders in information-based AI.

In line with its Metaverse ambitions, management has also directed the company toward virtual reality and augmented reality through its Reality Labs division. It has recently partnered with Rayban to release smart glasses, and it has a long-term vision to create a fully immersive Metaverse by 2030. If successful, the company could be pivotal in revolutionizing social interaction, remote work opportunities, education and entertainment, among other use cases.

Moving forward, the company will also be actively working on expanding its presence in emerging markets as internet adoption rates in less-developed regions grow exponentially. Management has structured an initiative called the Facebook Connectivity project, which aims to provide affordable internet access in underserved regions. This strategy is vital to help Meta tap into new user bases and will help it continue to sustain growth.

Meta recently initiated its first-ever dividend. It announced a cash dividend of 50 cents per share for both Class A and Class B common stock, which will be paid quarterly and began in March 2024. While the yield is only a modest 0.20% right now, this marks the start of an exciting new chapter for its shareholders.

As its payout ratio for the dividend is reasonably low, many analysts suggest management will increase the dividend payments in the future. I think this is going to attract a new market of investors, and while future growth might not be as bright as it once was during the company’s ascent, the prudent and gradual shift of financial strategy to favor income investors bodes very well for the stock’s long-term popularity.

However, the revenue growth and net income growth slowdown are likely to create some price volatility in the interim, especially as higher dividend yields are not likely to be initiated anytime soon. Currently, the share price is showing resistance, which, based on my experience, is reflective of the slower future fundamental growth estimates being priced in by the market.

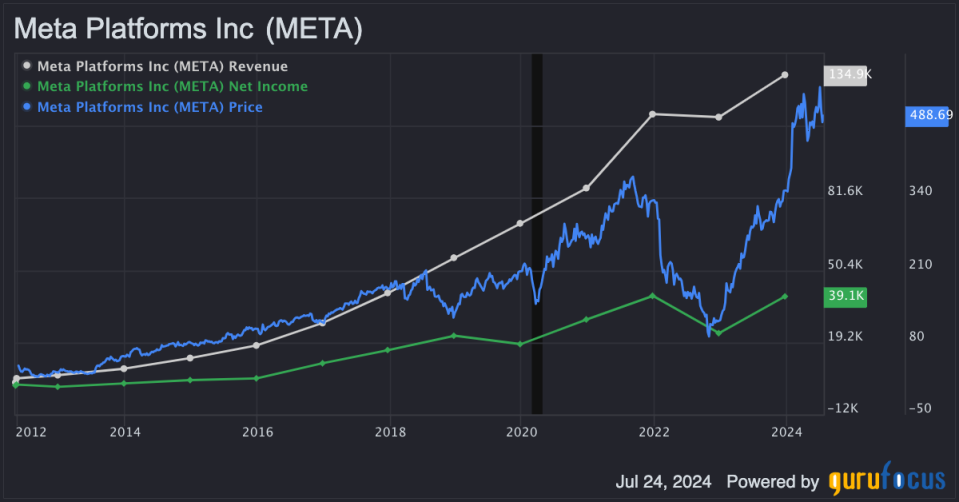

Meta has achieved 116% earnings per share without non-recurring items growth and 23% revenue growth over the past year, but the future three-year consensus analyst estimate is a 21% earnings per share without NRI growth rate and a 14% revenue growth rate, indicating the significant slowdown already being represented in the price. I think this is going to produce downside volatility based on the overvaluation indicated by the GF Value Line.

In other words, I think now is a poor time to invest in Meta. In addition, those who are not tolerant of some short-term downside may consider selling at the present levels and reallocating the capital to an undervalued stock. In effect, this strategy would be likely to deliver the highest alpha overall.

That being said, if one is keen to stay invested in Meta, long-term growth should be good despite any short-term downside from overvaluation and the dividend is a valid reason to stay invested over the next five to 10 years.

As a technology researcher, one of the elements about Meta that has come to my attention from listening to and reading the work of many Silicon Valley executives and experts from further afield is the company is developing somewhat of a bad reputation for the effects its products are having on people’s health. For example, research indicates the platforms can decrease social cohesion rather than increase it and also negatively impact brain health by having detrimental effects on dopamine production related to notifications. This is a problem I think is going to be brought to light more in the coming years, and I think if Meta does not work to address this issue more proactively, it could see a reduction in user engagement and experience fundamental contraction as a result.

That being said, Meta is working hard to try to address these issues and I have heard Mark Zuckerberg express his acknowledgments of these concerns myself. The company is investing in research to adapt its models to be safer and healthier. As an example of its proactivity, it has enabled parental controls in the form of 30 tools to help protect teens and give parents oversight over their children’s use of Meta’s services.

In addition, as Meta is becoming more aggressively focused on AI now, it is important to recognize how competitive this field is becoming. Other players, like OpenAI, Grok, Amazon (AMZN), Microsoft (NASDAQ:MSFT), Alphabet (NASDAQ:GOOGL) (NASDAQ:GOOG) and others, are likely to pose a threat to Meta’s market share. What I think Meta has going for it is that it has embedded its AI into its family of apps, which is a significant point of access. Further, unlike Apple (NASDAQ:AAPL), Meta has developed its own AI infrastructure and models, meaning it isn’t reliant on other major players like OpenAI for its capabilities. This opens up much more room for profit generation over the long term.

I am very confident in Meta’s long-term future despite the growing concerns related to health, which I think the company will address more proactively moving forward. I think as the company evolves it will become a lot more immersive, and the result of this should translate to retention of user engagement over time. As the community becomes fully formed and the market is fully saturated, Meta’s financial approach to offering dividends is very shrewd, and I think it has the potential to keep investors very pleased if it expands this dividend substantially in relativity to the slowing fundamental growth rates.

Meta is capable of evolving into a company that, over the long term, is seen as a net benefit to society rather than an issue to public health. While it has a history of bad press related to the negative effects of its apps, particularly on young people, the company’s moat is now much wider, so it has to compete less aggressively. Instead, its work is in maintaining its ecosystem. From listening to many interviews with Zuckerberg, I think he is going to focus on the reputational value of Meta rather than the pure monetization of its platforms and hours of user engagement. This could open up new revenue streams and be more conducive to long-term growth and sustenance than focusing on short-term earnings results.

This potential approach to ecosystem reputation, along with the dividend in the financial strategy, makes me very confident in the company’s long-term future potential, despite the short-term volatility I see as likely in the stock price over the next 12 months due to its potential overvaluation.

This article first appeared on GuruFocus.

link