Europe Breakfast Cereals Market Size and Analysis, 2033

Europe Breakfast Cereals Market Size

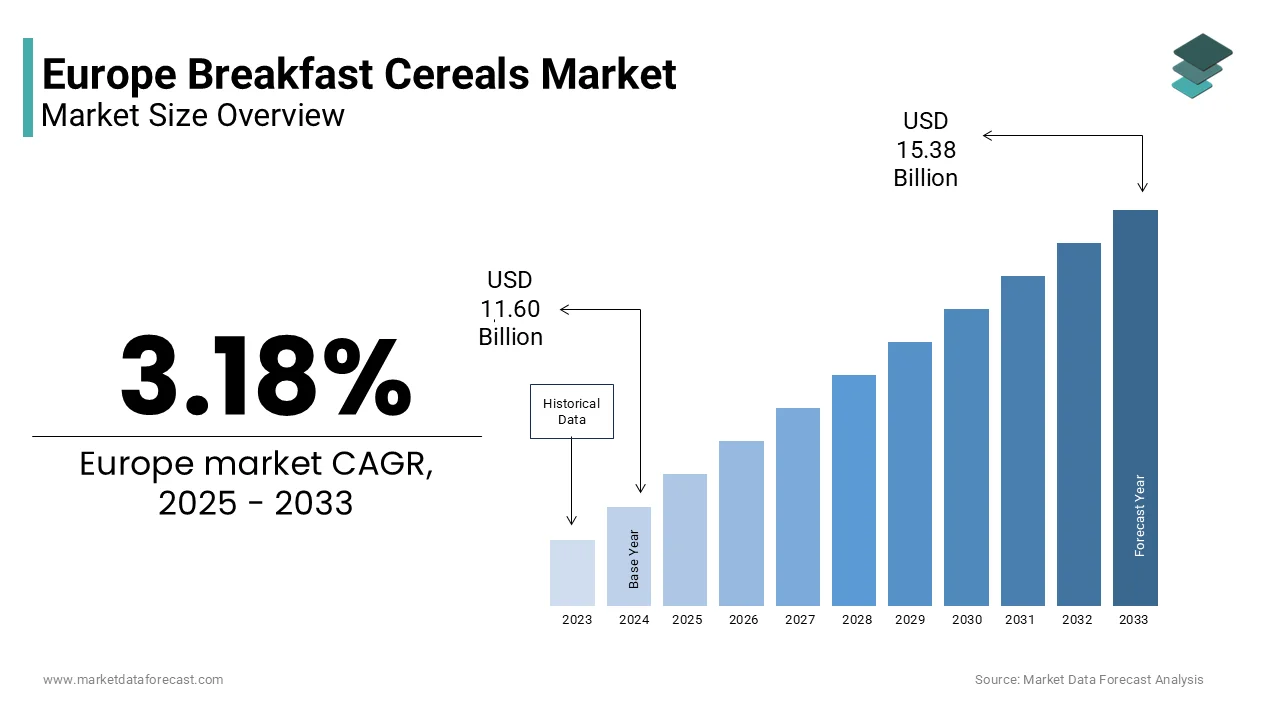

The Europe breakfast cereals market size was valued at USD 11.60 billion in 2024 and is projected to reach USD 15.38 billion by 2033 from USD 11.97 billion in 2025, growing at a CAGR of 3.18%.

The breakfast cereals are a diverse array of ready-to-eat grain-based products consumed predominantly during morning meals across European households. These products include flakes, muesli, granola, puffed grains, and fortified cereals, which are often marketed for their convenience, nutritional content, and alignment with evolving dietary preferences. The cultural emphasis on structured morning routines in many European countries continues to sustain consistent demand. According to Eurostat, over 78% of adults in the European Union consume breakfast on a daily basis, with breakfast cereals forming a significant portion of morning intake in countries such as Germany, the United Kingdom, and the Netherlands. As per the Food and Agriculture Organisation of the United Nations, average per capita consumption of breakfast cereals in Western Europe exceeds 3 kilograms annually, significantly higher than in Southern or Eastern regions. Urbanisation and time-constrained lifestyles further reinforce reliance on convenient breakfast solutions. Consumer interest in functional ingredients such as fibre, protein, and probiotics has also driven product diversification.

MARKET DRIVERS

Rising Demand for Functional and Fortified Cereal Variants

The growing number of consumers prioritising food products that deliver tangible health benefits beyond basic nutrition is a major factor propelling the growth of the European breakfast cereals market. Europe’s escalating public health focus on preventive nutrition in ageing populations seeking to manage chronic conditions, which is also boosting the growth of the market. According to the European Commission’s Joint Research Centre, many adults in the EU express willingness to choose foods enriched with vitamins, minerals, or fiber for improved digestive or cardiovascular health. Manufacturers have responded by integrating ingredients such as beta-glucans, plant-based proteins, and probiotics into cereal formulations. For instance, granola varieties fortified with omega-3 fatty acids or plant sterols have gained traction in Nordic and Benelux markets. Regulatory frameworks under the European Union’s Nutrition and Health Claims Regulation further enable transparent labelling, bolstering consumer trust.

Growing Adoption of Plant-Based and Clean Label Cereals

The consumer aversion to artificial additives and synthetic ingredients has robust demand for clean label breakfast cereals with plant-based formulations, among younger people is accelerating the growth of the European breakfast cereals market. Transparency in sourcing and simplicity in ingredient lists now rank among the top purchase criteria, which reflects a broader shift toward whole food diets. According to the European Consumer Organisation BEUC, some consumers in 2024 indicated they avoid products containing artificial colours, flavours, or preservatives, a sentiment especially pronounced in France, Sweden, and Austria. The cereal manufacturers are leveraging locally sourced grains and regenerative agricultural practices to appeal to eco-conscious buyers. Retailers like Edeka in Germany and Carrefour in France have expanded shelf space for clean-label cereals by over 30% since 2022, which is signalling strong commercial validation.

MARKET RESTRAINTS

Persistent Consumer Concerns Over Added Sugar Content

The high sugar content in many breakfast cereals remains a significant barrier to consumption growth, particularly as public health authorities intensify scrutiny on added sugars is restraining the growth of the European breakfast cereals market. According to a 2023 assessment by some research, nearly 40% of breakfast cereals marketed to children in the EU contain more than 20 grams of sugar per 100 grams, triggering regulatory and parental backlash. In response, countries like the United Kingdom and Portugal have implemented front-of-pack warning labels for high sugar products, directly impacting purchase decisions. Manufacturers face a delicate balancing act, where reducing sugar often compromises taste and texture, leading to consumer rejection.

Intensifying Competition from Alternative Breakfast Formats

The rising popularity of alternative breakfast formats such as yoghurtt bowls, smoothies, protein bars, and artisanal breads, which are increasingly perceived as fresher and more nutritious, is also a significant factor in the decline of the growth of the European breakfast cereals market. Urban consumers in metropolitan hubs like Berlin, Paris, and Amsterdam are gravitating toward oon-the-goor customised breakfast solutions that align with personalised nutrition trends. According to Euromonitor International, sales of ready-to-eat alternatives like oat cups and chia pudding grew by 18% annually between 2021 and 2024, outpacing traditional cereal categories. Additionally, the cafe culture revival post-pandemic has normalised breakfast consumption outside the home. This shift reflects bigger changes in meal structuring, where breakfast is no longer viewed as a standardised, at-home ritual but as a flexible, experience-driven occasion. Legacy cereal brands, constrained by shelf-stable formats and legacy marketing, struggle to replicate the perceived freshness and customisation offered by competitors.

MARKET OPPORTUNITIES

Expansion into Premium and Niche Health Segments

The premium and specialised health lines, as affluent and health literate consumers demonstrate willingness to pay higher prices for differentiated nutritional profiles, are a prominent factor in setting up new opportunities for the growth of the European breakfast cereals market. Products targeting specific dietary needs, such as gluten-free, keto-friendly, or high fibre formulations, are gaining commercial traction, supported by rising diagnosis rates of conditions like celiac disease and metabolic syndrome. According to the research, approximately 1% of the EU population suffers from celiac disease, while an additional 6% actively avoid gluten for perceived digestive benefits. Similarly, demand for high-protein cereals is accelerating; protein fortified breakfast products grew by 22% in Western Europe between 2022 and 2024, fueled by fitness-oriented demographics. Regulatory harmonisation under the EU’s Health Claims Regulation provides a structured pathway for substantiated messaging by enhancing consumer confidence.

Leveraging E Commerce and Direct-to-Consumer Channels for Personalisation

The rapid digitisation of grocery purchasing in Europe has unlocked new avenues for cereal brands to bypass traditional retail constraints and engage consumers through personalised, data-driven offerings. The leveraging of e-commerce and direct-to-consumer channels for personalisation is ascribed to bolstering the growth of the European breakfast cereals market. Online grocery penetration in the EU, with subscription-based models and customised cereal blends emerging as high-growth niches. Companies like MyMuesli in Germany and Eat Natural in the UK have built successful direct-to-consumer platforms, allowing customers to design cereals based on taste, dietary goals, and ingredient preferences. Social media and influencer partnerships further amplify reach among health-conscious millennials seeking transparency and authenticity. Digital channels also enable real-time feedback loops, accelerating product iteration. For example, a seasonal pumpkin seed and cranberry blend launched via Instagram polls achieved 15000 units sold within two weeks in France. Moreover, e-commerce reduces reliance on slotting fees and promotional discounts prevalent in brick-and-mortar retail by improving margin sustainability.

MARKET CHALLENGES

Volatile Pricing and Supply Chain Disruptions in Key Grain Inputs

The report contends with persistent volatility in the cost and availability of core grain inputs such as wheat, oats, and barley, driven by climatic instability and geopolitical pressures. The volatile pricing and supply chain disruptions in key grain inputs are also expected to pose a challenging factor for the growth of the European breakfast cereal market. The 2022 and 2023 growing seasons witnessed significant yield reductions across major EU cereal-producing regions. Concurrently, the ongoing conflict in Eastern Europe disrupted supply chains for sunflower seeds and maize, often used in composite cereal blends. These disruptions translated into raw material cost inflation, and wholesale oat prices surged by 28% between January 2022 and December 2023. For cereal manufacturers operating on narrow margins, such volatility compresses profitability and complicates long-term pricing strategies. While large multinationals may hedge against fluctuations, smaller regional brands lack the financial instruments to absorb shocks, leading to product discontinuities or market exits. Furthermore, consumer sensitivity to price increases, evidenced in a 2024 European switched to cheaper breakfast alternatives during inflation peaks, limits the ability to pass costs downstream.

Regulatory Fragmentation Across EU Member States on Nutrition Labelling

The significant disparities in national interpretations of nutrition labelling and health claims create operational complexity and compliance risks for breakfast cereal manufacturers operating across multiple countries. The regulatory fragmentation across EU member states on nutrition labelling is also hampering the growth of the European breakfast cereals market. While the EU’s Nutrition and Health Claims Regulation provides a common framework, individual member states enforce supplementary rules that can contradict or exceed baseline requirements. For example, France’s Nutri Score system assigns front-of-pack colour-coded ratings based on algorithmic calculations, whereas Germany permits specific nutrient content claims if substantiated, and Italy requires additional warnings for products high in sugar marketed to children. These inconsistencies confuse consumers and dilute brand messaging; as per a 2024 study by the University of Wageningen, 58% of cross-border shoppers in the EU struggle to compare nutritional value across similar cereal products due to differing label formats. Moreover, the European Court of Auditors has criticised the lack of enforcement uniformity, noting that health claims approved in one country may be challenged in another. This regulatory patchwork impedes economies of scale, discourages SMEs from pan-European expansion, and delays innovation cycles as companies navigate legal ambiguities.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 to 2033 |

|

Base Year |

2024 |

|

Forecast Period |

2025 to 2033 |

|

CAGR |

3.18% |

|

Segments Covered |

By Type, Ingredient Source, Packaging, Type, Distribution Channel, Age Group, and Region |

|

Various Analyses Covered |

Global, Regional, & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

|

Regions Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

|

Market Leaders Profiled |

Kellogg’s (US), General Mills (US), Nestlé (CH), Post Holdings (US), Quaker Oats Company (US), Cereal Partners Worldwide (CH), Weetabix (GB), PepsiCo (US), Sunrise Foods (IN) |

SEGMENTAL ANALYSIS

By Type Insights

The Ready to Eat Cereals segment accounted in holding a dominant share of the European Breakfast Cereals market in 2024. The rapid pace of urban life across Europe has entrenched convenience as a non-negotiable criterion in food selection. Ready-to-Eat Cereals require no preparation other than pouring milk or a plant-based alternative, which makes them ideal for time-pressed professionals and school-going children. A 2024 consumer behaviour study by GfK across 12 European countries revealed that 68% of breakfast cereal purchasers prioritise speed of preparation above all else, with Ready to Eat options cited as the top choice in households with dual income earners. Germany, France, and three of Europe’s largest cereal-consuming nations report average weekday breakfast durations of just seven minutes. This behavioural shift has rendered traditional cooked porridges or oatmeals less viable for daily consumption despite their nutritional merits. Retailers reinforce this trend by allocating prime shelf space to Ready to Eat variants, further solidifying their dominance.

The Ready to Cook Cereals segment is likely to grow the fastest CAGR of 5.8% from 2025 to 2033. A growing segment of European consumers is rejecting ultra-processed foods in favour of ingredients perceived as authentic and nutritionally intact. Ready-to-cook cereals, such as steel-cut oats, whole barley flakes, and unhulled millet, align with this “clean kitchen” philosophy. National dietary guidelines in countries like Sweden and Switzerland now explicitly recommend minimally processed grains for glycemic control, further legitimising this shift.

Ready-to-Cook Cereals are experiencing renewed relevance through cultural reappropriation and artisanal food trends. In Eastern and Southern Europe, traditional hot cereals like Italian farro porridge or Czech kase are being rebranded as heritage superfoods. As per the Slow Food Foundation, sales of heritage grain-based hot cereals in Italy and Hungary grew by 17% in 2024, driven by farm-to-table tourism and food education initiatives. Social media further amplifies this trend; #RealBreakfast posts featuring stovetop oatmeal or spelt porridge garnered over 3.2 million engagements across EU platforms in 2024. This cultural renaissance transforms Ready to Cook cereals from utilitarian staples into symbols of culinary authenticity, attracting premium pricing and younger demographics seeking meaningful food experiences beyond convenience.

By Ingredient Source Insights

The ingredient source segment was the largest by accounting for 38.3% of the European breakfast cereals market in 2024. Wheat’s deep integration into Europe’s agricultural economy and food manufacturing systems. The EU produces over 125 million metric tons of wheat annually, with France, Germany, and Poland ranking among the top five global exporters. This abundant supply ensures price stability and consistent quality for cereal producers. Moreover, wheat’s functional properties its gluten content, make it ideal for extrusion and flaking processes used in most Ready to Eat cereals. As per the survey, over 70% of European cereal production lines are optimised for wheat-based formulations by creating significant switching costs for manufacturers. Consumer familiarity also plays a role, where a 2024 Mintel survey across six major EU countries respondents associate “classic breakfast cereal” with wheat flakes or biscuits. National bread cultures further normalise wheat as a daily grain, reinforcing its acceptability in breakfast contexts. Regulatory approvals for wheat-based health claims, such as those related to whole grain content under EFSA, are also more advanced than for alternative grains, facilitating compliant marketing.

The oats segment is lucratively to witness a fastest CAGR of 7.2% from 2025 to 2033. Oats’ meteoric rise is anchored in robust clinical validation of their soluble fibre beta-glucan, which is proven to lower LDL cholesterol and support glycemic control. The European Food Safety Authority authorised a specific health claim in 2011 stating that “3 grams of beta-glucan from oats per day contributes to the maintenance of normal blood cholesterol levels,” a message now widely featured on packaging across the EU. Retail sales data from NielsenIQ shows oat cereals outperforming the overall category by 14%age points in 2024. National health bodies like Germany’s Federal Centre for Nutrition actively promote oat consumption, further legitimising its status.

By Distribution Channel Insights

The supermarkets and hypermarkets segment was the largest by capturing a dominant share of the European breakfast cereals market in 2024. The growth of the segment is likely to be driven by their ability to offer extensive product variety, aggressive pricing, and high-impact promotional placements. These retailers control over 75% of total packaged food sales in Western Europe, as noted by the European Retail Round Table. Weekly promotions on breakfast cereals that are often bundled with milk or yoghurt drive bulk purchasing. Moreover, private label development is almost exclusively concentrated in this channel, with store brands accounting for 41% of cereal sales in hypermarkets across Germany and the Netherlands. The physical layout of these stores features dedicated breakfast aisles at eye level that reinforce habitual purchasing. This combination of economic leverage, consumer reach, and behavioural engineering makes supermarkets the default channel for both established and emerging brands.

The online sales segment is expected to grow at the fastest CAGR of 11.4% from 2025 to 2033. Digital platforms now enable recurring deliveries and customised cereal blends tailored to dietary preferences, allergies, or health goals. Companies like MyMuesli and Oatly’s digital arm have built subscription ecosystems where consumers design cereals with precise macronutrient profiles. As per McKinsey’s 2024 European E Commerce Tracker, online cereal buyers opt for subscription services, citing convenience and consistency as key drivers. These models foster brand loyalty far beyond one-off purchases; customer retention rates exceed 70% after six months, compared to 45% in traditional retail. The integration of AI-driven recommendations based on past orders or health app data further enhances relevance.

REGIONAL ANALYSIS

Germany Breakfast Cereals Market Analysis

Germany was the top performer of the European breakfast cereals market by holding 19.2% of share in 2024, with its deeply ingrained breakfast culture and robust domestic production ecosystem. Germans consume an average of 4.1 kilograms of breakfast cereals per capita annually, the highest in the EU, as per some research. This high penetration is sustained by a strong tradition of muesli and granola consumption, particularly in southern regions where homemade blends remain popular. The country’s health-conscious populace actively seeks high fibre, low sugar options, prompting brands like Verival and Alnatura to pioneer clean label innovations. Regulatory alignment with EFSA health claims has enabled widespread use of fibre and whole grain messaging, further boosting trust. Additionally, Germany’s dense retail network with over 38000 supermarkets and organic stores ensures ubiquitous availability.

United Kingdom Breakfast Cereals Market Analysis

The United Kingdom was ranked second by capturing 15.8% of Europe’s breakfast cereals market share in 2024, driven by a mature branded cereal market and consistent breakfast consumption patterns despite evolving dietary trends. According to the UK’s National Diet and Nutrition Survey, 68% of adults consume breakfast daily, with Ready to Eat cereals present in over half of these occasions. Kellogg’s and Nestlé have maintained a stronghold through decades of advertising and school nutrition partnerships, although recent sugar reduction mandates have prompted significant reformulation. Public Health England’s sugar reduction program contributed to a 20% decline in average sugar content across top cereal brands between 2015 and 2023. Simultaneously, private label growth has accelerated, and Tesco and Sainsbury’s now account for 33% of total cereal sales by offering value-driven alternatives. The rise of plant-based diets has also expanded demand for fortified oat and rice cereals, with sales increasing by 18% in 2024.

France Breakfast Cereals Market Analysis

The French breakfast cereals market is likely to grow at the fastest CAGR from 2025 to 2033, with its preference for artisanal and organic cereal blends, mass-produced flakes. French consumers exhibit high sensitivity to ingredient origin and processing methods, with 57% preferring cereals labelled “sans sucres ajoutés” (no added sugars), as per INSEE’s 2024 household consumption survey. The country’s muesli culture, influenced by Alpine wellness traditionsfavoursrs mixtures with dried fruits, seeds, and regional grains like spelt. Carrefour and Leclerc have responded by dedicating entire shelves to organic and locally sourced cereals, which now represent 41% of the cereal category in hypermarkets, according to FranceAgriMer. Regulatory support through the Nutri Score system has further shaped demand; cereals scoring A or B receive preferential placement and promotional support. Additionally, school breakfast programs in underserved regions funded by the Ministry of Education have increased household trial of fortified variants.

Italy Breakfast Cereals Market Analysis

Italy’s breakfast cereals market growth is likely to grow with a dual consumption pattern that blends traditional hot cereals with growing interest in modern granola formats. While breakfast cereal penetration historically lagged behind Northern Europe, urbanisation has accelerated adoption, particularly among millennials in cities like Milan and Rome. Italian consumers favour crunchynut-based granolas with Mediterranean ingredients such as almonds, figs, and extra virgin olive oil drizzle products that align with the national diet’s emphasis on whole foods. Brands like Esselunga’s private label and Balocco have capitalised on this by launching regionally inspired blends. Furthermore, the rise of coffee bar culture has normalised “colazione da asporto” (takeaway breakfast), where granola cups paired with yoghurts are increasingly common.

Spain Breakfast Cereals Market Analysis

Spain’s breakfast cereals market growth is driven by the rising health awareness and breakfast modernisation. Traditionally dominated by bread and olive oil, Spanish morning routines are shifting toward lighter, faster options, especially in dual-income households. Corn and rice-based cereals that are often gluten-free are particularly popular, catering to Spain’s relatively high celiac prevalence of 1.3%. Retailers like Mercadona have driven accessibility through affordable private label ranges, which now constitute 48% of cereal sales. Additionally, government-backed school breakfast initiatives in regions like Catalonia have introduced fortified cereals to children, fostering early brand familiarity.

COMPETITIVE LANDSCAPE

Competition in the European breakfast cereals market is characterised by intense rivalry among multinational corporations and agile regional brands. Established players leverage strong distribution networks, brand heritage, and extensive R and D capabilities to maintain relevance amid shifting dietary norms. Simultaneously, niche producers gain traction by offering organic, gluten-free, or functional cereals that cater to specific health needs. Price sensitivity in Southern and Eastern Europe intensifies pressure on private label offerings from major retailers. Innovation cycles have accelerated as companies race to meet demands for sustainability, transparency, and personalisation. Regulatory compliance across diverse national labelling systems adds complexity, requiring significant legal and operational resources. The market also faces disruption from alternative breakfast formats, compelling incumbents to diversify beyond traditional flakes.

KEY MARKET PLAYERS

Some of the notable key players in the European breakfast cereals market are

- Kellogg’s (US)

- General Mills (US)

- Nestlé (CH)

- Post Holdings (US)

- Quaker Oats Company (US)

- Cereal Partners Worldwide (CH)

- Weetabix (GB)

- PepsiCo (US)

- Sunrise Foods (IN)

Top Players in the Market

- Nestlé holds a prominent position in the European breakfast cereals market through its Cereal Partners Worldwide joint venture with General Mills. The company emphasises nutritional innovation by progressively reducing sugar content and introducing high-protein and fibre-enriched variants. In recent years, Nestlé has accelerated its investment in plant-based and organic cereal lines to align with European consumer preferences for clean-label products. It has also integrated regenerative agriculture principles into its oat and wheat sourcing across Scandinavia and France. These initiatives reinforce its commitment to sustainability while meeting evolving dietary demands across diverse European markets.

- Kellogg’s maintains strong brand recognition in Europe with a portfolio spanning traditional flakes to premium granolas under brands like Special K and All Bran. The company has intensified its focus on transparency by simplifying ingredient lists and removing artificial additives. Recent efforts include launching recyclable packaging across its European operations and expanding its direct-to-consumer platform with personalised cereal blends. Kellogg’s has also collaborated with local farmers to secure non-GMO grain supplies in Germany and Italy. These actions demonstrate its strategy of combining heritage trust with modern health and environmental values.

- General Mills participates in the European breakfast cereals market primarily through its partnership with Nestlé but also via independent brands like Nature Valley. The company has prioritised portfolio diversification by introducing ancient grain and gluten-free cereals tailored to European taste profiles. It has enhanced its digital engagement through social media campaigns promoting mindful breakfast routines and partnered with fitness influencers in the UK and Sweden. General Mills also invests in consumer education on whole-grain benefits through collaborations with European nutrition societies. These moves reflect its broader mission to position cereals as a functional component of balanced lifestyles.

Top Strategies Used by the Key Market Players

Key players in the European breakfast cereals market prioritise product reformulation to reduce sugar and enhance nutritional profiles in response to stringent public health guidelines. They invest heavily in clean label innovation by eliminating artificial ingredients and incorporating whole grains, seeds, and plant-based proteins. Strategic partnerships with local farmers ensure traceable and sustainable grain sourcing aligned with the European Green Deal. Companies expand direct-to-consumer channels through personalised subscription models and e-commerce platforms. They also leverage digital marketing and influencer collaborations to engage health-conscious millennials and Gen Z consumers across urban centres.

MARKET SEGMENTATION

This research report on the European breakfast cereals market has been segmented and sub-segmented based on categories.

By Type

- Ready-To-Eat Cereals

- Ready-To-Cook Cereals

By Ingredient Source

- Wheat

- Corn

- Oats

- Rice

- Barley

- Others

By Packaging Type

- Boxes

- Stand-Up Pouches

- More packaging types

By Distribution Channel

- Supermarkets/Hypermarkets

- Convenience/Grocery Stores

- Other channels

By Age Group

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

link