Microsoft’s Strong Q4 Earnings: What It Means For Your Investment Strategy (NASDAQ:MSFT)

")

Jean-Luc Ichard

Investment Thesis

On 30th July, Microsoft Corporation (NASDAQ:MSFT) released its FY24 Q4 earnings results. The company reported a revenue of $64.7B, an increase of 15% compared to the same quarter in the previous year. Additionally, Microsoft reported a net income of $22B, up 10% compared to FY23 Q4.

Microsoft announced diluted earnings per share of $2.95, an increase of 10% compared to the same quarter in the previous year, highlighting the company’s potential for dividend growth.

Microsoft’s strong earnings results in FY24 Q4 reinforce my current buy rating for the company. Despite Microsoft’s slightly elevated valuation, I consider Microsoft to be fairly valued. This is the case since Microsoft’s current valuation is only slightly above its 5-year Average. I am convinced that Microsoft should be rated at a premium when compared to other companies in the Information Technology Sector due to its robust competitive position, significant competitive advantages, and strong financial health.

I believe that the company is particularly attractive for young investors who aim to invest with a long investment horizon and who plan to benefit from the company’s strong dividend growth potential (underlined by Microsoft’s 10-Year Dividend Growth Rate [CAGR] of 10.60%).

It is worth highlighting that last week, on 23rd July, Microsoft competitor Alphabet Inc. (GOOG)(GOOGL) aka Google had already reported its latest earnings results. Alphabet announced quarterly revenues of $84.7B, which was an increase of 14% year-over-year, underlying the company’s positive growth outlook.

Both Microsoft and Alphabet are key players in The Dividend Income Accelerator Portfolio, effectively contributing by optimizing the portfolio in terms of risk and reward. I also expect both companies to significantly contribute to the portfolio’s dividend growth potential in the years ahead.

I particularly suggest younger investors should overweight Microsoft in an investment portfolio and maintain a long-term investment focus to benefit from the company’s attractive risk-reward profile and its strong ability to contribute to your portfolio’s dividend growth potential. However, given the company’s elevated downside risk, which is a result of its elevated valuation, I propose setting an allocation limit of 5% in relation to your overall investment portfolio. This strategic approach allows you to increase the likelihood of reaching a positive Total Return with your overall portfolio.

Microsoft’s Current Valuation

I believe that Microsoft is currently fairly valued. This is the case since the company’s P/E [FWD] Ratio of 35.39 is only slightly above its average from the past five years (which is 31.22) and only slightly above the Sector Median of 29.48.

However, it is important to highlight that I believe Microsoft should be rated with a premium when compared to most of its competitors in the Information Technology Sector. This is due to the company’s strong competitive advantages, its broad and diversified product portfolio, and its leading market position within its sector. Therefore, I believe that Microsoft is currently fairly valued, even though its valuation is slightly above the Sector Median.

Microsoft’s Growth Outlook

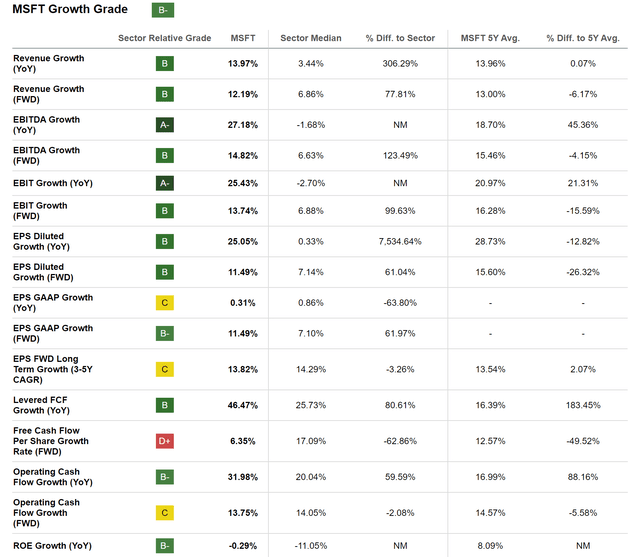

Microsoft’s positive growth outlook is underlined by a Seeking Alpha Growth Grade of B- for the company. This confirms Microsoft’s excellent growth prospects and underscores my current buy rating for the company.

Microsoft’s EBITDA Growth Rate [FWD] stands at 14.82%, which is 123.49% above the Sector Median. This indicates that Microsoft has been able to increase its earnings more than its competitors.

It is also worth highlighting Microsoft’s EPS Diluted Growth Rate [FWD] of 11.49%, which is 61.04% above the Sector Median, underscoring Microsoft’s strong potential to increase its dividend.

Source: Seeking Alpha

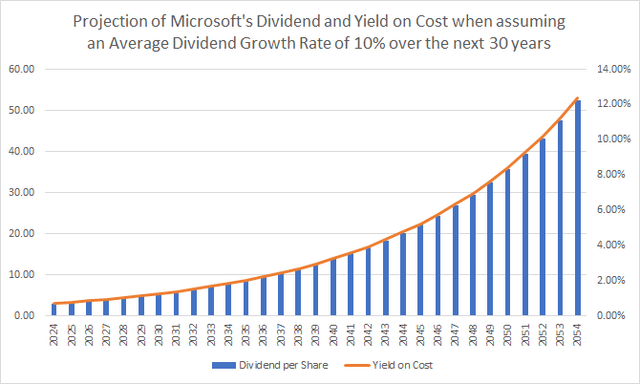

Microsoft’s Dividend Growth Potential and the Projection of its Dividend and Yield on Cost

I am convinced that Microsoft still has strong potential for dividend growth in the years ahead. This is not just based on the company’s 10-Year Dividend Growth Rate [CAGR] of 10.60% but also on its EPS Diluted Growth Rate [FWD] of 11.49%.

The chart below illustrates a projection of Microsoft’s Dividend and Yield on Cost if it is assumed that the company was able to raise its dividend by 10% per year for the following 30 years (which is based on the above growth rates).

Source: The Author

Assuming these dividend growth rates and that you invest in Microsoft at the company’s current stock price of $423.78, you could potentially reach a Yield on Cost of 1.84% in 2034, 4.76% in 2044, and 12.35% in 2054. These numbers underline Microsoft’s strong dividend growth potential.

These dividend enhancements could be a potential driver for the company’s increasing stock price in the years ahead. In such a case, you would benefit not only from the company’s steadily increasing dividend payments but also from capital appreciation.

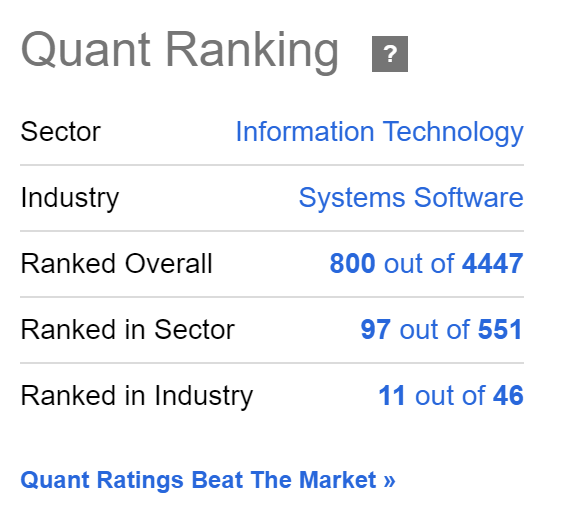

Microsoft, according to the Seeking Alpha Quant Ranking

According to the Seeking Alpha Quant Ranking, Microsoft is presently ranked 11th out of 46 within the Systems Software Industry. The company is also ranked 97th out of 551 within the Information Technology Sector and 800th out of 4,447 within the overall ranking. The Seeking Alpha Quant Ranking for Microsoft underlines my buy rating for the company.

Source: Seeking Alpha

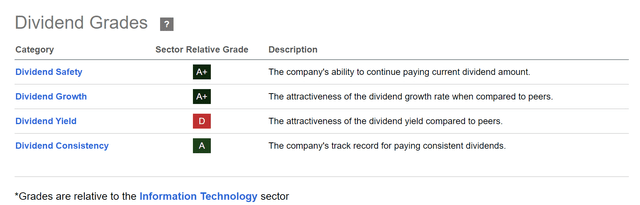

Microsoft, according to the Seeking Alpha Dividend Grades

The Seeking Alpha Dividend Grades reinforce my belief that Microsoft is an excellent pick for those investors focusing on dividend growth. The company receives an A+ for Dividend Safety and Dividend Growth and an A for Dividend Consistency. For Dividend Yield, Microsoft receives a D rating.

Source: Seeking Alpha

Why I have added Microsoft to The Dividend Income Accelerator Portfolio

About 11 months ago, I started building The Dividend Income Accelerator Portfolio. I am constantly documenting and optimizing the portfolio here on Seeking Alpha to ensure a constantly reduced portfolio risk level, which allows us to have a high probability of reaching attractive investment outcomes.

The portfolio’s primary objective is reaching a balance between dividend income and dividend growth, helping investors generate an attractive dividend income for today while constantly raising this amount.

Microsoft is an important element of The Dividend Income Accelerator Portfolio, currently representing 1.94% of the overall portfolio. I added Microsoft to the portfolio due to its ability to provide the portfolio with significant dividend growth (evidenced by the company’s 10-Year Dividend Growth Rate [CAGR] of 10.60%), its financial health (Aaa credit rating from Moody’s), strong competitive advantages, and its positive growth prospects, which have been underscored by Microsoft’s strong FY24 Q4 earnings results.

It is further worth highlighting that Microsoft competitor Alphabet, which reported its latest earnings results last week, is also a strategically significant core element of The Dividend Income Accelerator Portfolio. Like Microsoft, I believe that Alphabet is an attractive risk-reward choice for investors and will contribute to the portfolio’s dividend growth potential. I expect both companies to contribute significantly to the portfolio, reaching an attractive Total Return.

The Main Risk Factor When Investing in Microsoft and How to Reduce This Risk

In my opinion, the main risk factor Microsoft investors should consider is the company’s slightly elevated valuation. Currently, the company exhibits a P/E [FWD] Ratio of 35.39, indicating that elevated growth expectations are priced into the company’s share price. This leads to an elevated downside risk for Microsoft’s stock price that investors should be aware of.

To reduce this elevated downside risk of Microsoft’s stock price, investors should invest over the long term, with an investment horizon of at least five years. This ensures a reduction in the impact of any potential decline in the company’s stock price, which could result if Microsoft doesn’t meet its growth expectations.

I believe that investors who aim to prioritize dividend growth in their investment portfolios should consider overweighting Microsoft stock and positioning the portfolio for increased dividend growth potential.

However, I suggest setting the allocation limit to 5% for the Microsoft stock in relation to your overall investment portfolio. This allows you to reduce the portfolio’s downside risk and the portfolio’s company-specific allocation risk, thereby increasing the likelihood of positive investment results.

An additional risk factor includes Microsoft’s intense competition with other tech companies such as Alphabet, Amazon.com, Inc. (AMZN) and Apple Inc. (AAPL). In particular, Microsoft’s cloud computing platform Azure is in intense competition with the Amazon Web Services Platform and the Google Cloud Platform, which can adversely affect Microsoft’s financial results, especially in the short term, highlighting my long-term investment approach.

Conclusion

Microsoft’s strong FY24 Q4 earnings results have strengthened my belief in currently rating the company as a buy. Microsoft released diluted earnings per share of $2.95, an increase of 10% when compared to the same quarter in the year before.

Despite Microsoft’s slightly elevated valuation, I believe that the company is still fairly valued. Microsoft’s current valuation is only slightly above its 5-Year Average.

I particularly suggest that younger investors aiming to invest with a long investment horizon consider overweighting the Microsoft position in their investment portfolio to position their portfolio for increased dividend growth potential. This approach helps to increase the annual dividend payment you receive from the selected companies in your portfolio to a higher degree.

However, investors should be aware that Microsoft’s elevated valuation represents a downside risk for an investment portfolio, particularly over the short term. This underscores the importance of a long-term investment approach and an allocation limit. I recommend a 5% allocation limit for the Microsoft position. This ensures the reduction of the downside risk of your overall investment portfolio.

Microsoft is not only part of The Dividend Income Accelerator Portfolio. It is also among the largest positions in my personal investment portfolio. The same is true for Alphabet, which reported its earnings results a week ago.

When following a long-term approach, I am convinced that both Microsoft and Alphabet can be important strategic core positions for your investment portfolio, contributing to significant dividend growth and capital appreciation.

link